For almost two decades, managers have been learning to play by a new

set of rules. Companies must be flexible to respond rapidly to

competitive and market changes. They must benchmark continuously to

achieve best practice. They must outsource aggressively to gain

efficiencies. And they must nurture a few core competencies in race

to stay ahead of rivals.

Positioning—once the heart of strategy—is rejected as too static for

today’s dynamic markets and changing technologies. According to the

new dogma, rivals can quickly copy any market position, and

competitive advantage is, at best, temporary.

But those beliefs are dangerous half-truths, and they are leading

more and more companies down the path of mutually destructive

competition. True, some barriers to competition are falling as

regulation eases and markets become global. True, companies have

properly invested energy in becoming leaner and more nimble. In many

industries, however, what some call hypercompetition is a

self-inflicted wound, not the inevitable outcome of a changing

paradigm of competition.

The root of the problem is the failure to distinguish between

operational effectiveness and strategy. The quest for productivity,

quality, and speed has spawned a remarkable number of management

tools and techniques: total quality management, benchmarking,

time-based competition, outsourcing, partnering, reengineering,

change management. Although the resulting operational improvements

have often been dramatic, many companies have been frustrated by

their inability to translate those gains into sustainable

profitability. And bit by bit, almost imperceptibly, management

tools have taken the place of strategy. As managers push to improve

on all fronts, they move farther away from viable competitive

positions.

i

Operational effectiveness and strategy are both essential to

superior performance, which, after all, is the primary goal of any

enterprise. But they work in very different ways.

A company can outperform rivals only if it can establish a

difference that it can preserve. It must deliver greater value to

customers or create comparable value at a lower cost, or do both.

The arithmetic of superior profitability then follows: delivering

greater value allows a company to charge higher average unit prices;

greater efficiency results in lower average unit costs.

Ultimately, all differences between companies in cost or price

derive from the hundreds of activities required to create, produce,

sell, and deliver their products or services, such as calling on

customers, assembling final products, and training employees. Cost

is generated by performing activities, and cost advantage arises

from performing particular activities more efficiently than

competitors. Similarly, differentiation arises from both the choice

of activities and how they are performed. Activities, then are the

basic units of competitive advantage. Overall advantage or

disadvantage results from all a company’s activities, not only a

few.1

Operational effectiveness (OE) means performing similar activities

better than rivals perform them. Operational effectiveness includes

but is not limited to efficiency. It refers to any number of

practices that allow a company to better utilize its inputs by, for

example, reducing defects in products or developing better products

faster. In contrast, strategic positioning means performing

different activities from rivals’ or performing similar activities

in different ways.

Differences in operational effectiveness among companies are

pervasive. Some companies are able to get more out of their inputs

than others because they eliminate wasted effort, employ more

advanced technology, motivate employees better, or have greater

insight into managing particular activities or sets of activities.

Such differences in operational effectiveness are an important

source of differences in profitability among competitors because

they directly affect relative cost positions and levels of

differentiation.

Differences in operational effectiveness were at the heart of the

Japanese challenge to Western companies in the 1980s. The Japanese

were so far ahead of rivals in operational effectiveness that they

could offer lower cost and superior quality at the same time. It is

worth dwelling on this point, because so much recent thinking about

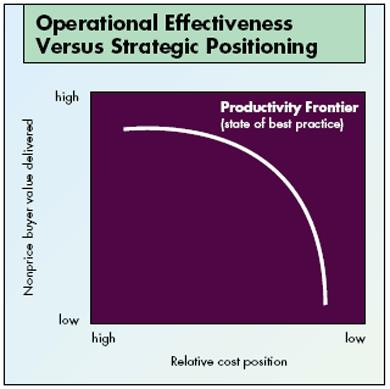

competition depends on it. Imagine for a moment a productivity

frontier that constitutes the sum of all existing best practices at

any given time. Think of it as the maximum value that a company

delivering a particular product or service can create at a given

cost, using the best available technologies, skills, management

techniques, and purchased inputs. The productivity frontier can

apply to individual activities, to groups of linked activities such

as order processing and manufacturing, and to an entire company’s

activities. When a company improves its operational effectiveness,

it moves toward the frontier. Doing so may require capital

investment, different personnel, or simply new ways of managing.

The productivity frontier is constantly shifting outward as new

technologies and management approaches are developed and as new

inputs become available. Laptop computers, mobile communications,

the Internet, and software such as Lotus Notes, for example, have

redefined the productivity frontier for sales-force operations and

created rich possibilities for linking sales with such activities as

order processing and after-sales support. Similarly, lean

production, which involves a family of activities, has allowed

substantial improvements in manufacturing productivity and asset

utilization.

For at least the past decade, managers have been preoccupied with

improving operational effectiveness. Through programs such as TQM,

time-based competition, and benchmarking, they have changed how they

perform activities in order to eliminate inefficiencies, improve

customer satisfaction, and achieve best practice. Hoping to keep up

with shifts in the productivity frontier, managers have embraced

continuous improvement, empowerment, change management, and the

so-called learning organization. The popularity of outsourcing and

the virtual corporation reflect the growing recognition that it is

difficult to perform all activities as productively as specialists.

As companies move to the frontier, they can often improve on

multiple dimensions of performance at the same time. For example,

manufacturers that adopted the Japanese practice of rapid

changeovers in the 1980s were able to lower cost and improve

differentiation simultaneously. What were once believed to be real

trade-offs—between defects and costs, for example—turned out to be

illusions created by poor operational effectiveness. Managers have

learned to reject such false trade-offs.

Constant improvement in operational effectiveness is necessary to

achieve superior profitability. However, it is not usually

sufficient. Few companies have competed successfully on the basis of

operational effectiveness over an extended period, and staying ahead

of rivals gets harder every day. The most obvious reason for that is

the rapid diffusion of best practices. Competitors can quickly

imitate management techniques, new technologies, input improvements,

and superior ways of meeting customers’ needs. The most generic

solutions—those that can be used in multiple settings—diffuse the

fastest. Witness the proliferation of OE techniques accelerated by

support from consultants.

OE competition shifts the productivity frontier outward, effectively

raising the bar for everyone. But although such competition produces

absolute improvement in operational effectiveness, it leads to

relative improvement for no one. Consider the $5 billion-plus U.S.

commercial-printing industry. The major players—R.R. Donnelley &

Sons Company, Quebecor, World Color Press, and Big Flower Press—are

competing head to head, serving all types of customers, offering the

same array of printing technologies (gravure and web offset),

investing heavily in the same new equipment, running their presses

faster, and reducing crew sizes. But the resulting major

productivity gains are being captured by customers and equipment

suppliers, not retained in superior profitability. Even

industry-leader Donnelley’s profit margin, consistently higher than

7% in the 1980s, fell to less than 4.6% in 1995. This pattern is

playing itself out in industry after industry. Even the Japanese,

pioneers of the new competition, suffer from persistently low

profits. (See the insert “Japanese Companies Rarely Have

Strategies.”)

i

The second reason that improved operational effectiveness is

insufficient—competitive convergence—is more subtle and insidious.

The more benchmarking companies do, the more they look alike. The

more that rivals outsource activities to efficient third parties,

often the same ones, the more generic those activities become. As

rivals imitate one another’s improvements in quality, cycle times,

or supplier partnerships, strategies converge and competition

becomes a series of races down identical paths that no one can win.

Competition based on operational effectiveness alone is mutually

destructive, leading to wars of attrition that can be arrested only

by limiting competition.

The recent wave of industry consolidation through mergers makes

sense in the context of OE competition. Driven by performance

pressures but lacking strategic vision, company after company has

had no better idea than to buy up its rivals. The competitors left

standing are often those that outlasted others, not companies with

real advantage.

After a decade of impressive gains in operational effectiveness,

many companies are facing diminishing returns. Continuous

improvement has been etched on managers’ brains. But its tools

unwittingly draw companies toward imitation and homogeneity.

Gradually, managers have let operational effectiveness supplant

strategy. The result is zero-sum competition, static or declining

prices, and pressures on costs that compromise companies’ ability to

invest in the business for the long term.

i

Competitive strategy is about being different. It means deliberately

choosing a different set of activities to deliver a unique mix of

value.

Southwest Airlines Company, for example, offers short-haul,

low-cost, point-to-point service between midsize cities and

secondary airports in large cities. Southwest avoids large airports

and does not fly great distances. Its customers include business

travelers, families, and students. Southwest’s frequent departures

and low fares attract price-sensitive customers who otherwise would

travel by bus or car, and convenience-oriented travelers who would

choose a full-service airline on other routes.

Most managers describe strategic positioning in terms of their

customers: “Southwest Airlines serves price- and

convenience-sensitive travelers,” for example. But the essence of

strategy is in the activities—choosing to perform activities

differently or to perform different activities than rivals.

Otherwise, a strategy is nothing more than a marketing slogan that

will not withstand competition.

A full-service airline is configured to get passengers from almost

any point A to any point B. To reach a large number of destinations

and serve passengers with connecting flights, full-service airlines

employ a hub-and-spoke system centered on major airports. To attract

passengers who desire more comfort, they offer first-class or

business-class service. To accommodate passengers who must change

planes, they coordinate schedules and check and transfer baggage.

Because some passengers will be traveling for many hours,

full-service airlines serve meals.

Southwest, in contrast, tailors all its activities to deliver

low-cost, convenient service on its particular type of route.

Through fast turnarounds at the gate of only 15 minutes, Southwest

is able to keep planes flying longer hours than rivals and provide

frequent departures with fewer aircraft. Southwest does not offer

meals, assigned seats, interline baggage checking, or premium

classes of service. Automated ticketing at the gate encourages

customers to bypass travel agents, allowing Southwest to avoid their

commissions. A standardized fleet of 737 aircraft boosts the

efficiency of maintenance.

Southwest has staked out a unique and valuable strategic position

based on a tailored set of activities. On the routes served by

Southwest, a full-service airline could never be as convenient or as

low cost.

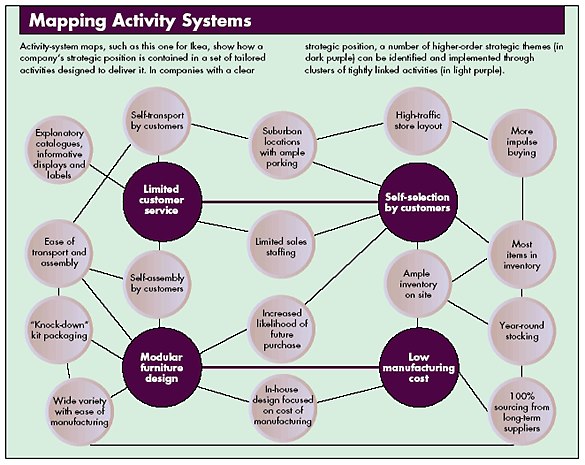

Ikea, the global furniture retailer based in Sweden, also has a

clear strategic positioning. Ikea targets young furniture buyers who

want style at low cost. What turns this marketing concept into a

strategic positioning is the tailored set of activities that make it

work. Like Southwest, Ikea has chosen to perform activities

differently from its rivals.

Consider the typical furniture store. Showrooms display samples of

the merchandise. One area might contain 25 sofas; another will

display five dining tables. But those items represent only a

fraction of the choices available to customers. Dozens of books

displaying fabric swatches or wood samples or alternate styles offer

customers thousands of product varieties to choose from. Salespeople

often escort customers through the store, answering questions and

helping them navigate this maze of choices. Once a customer makes a

selection, the order is relayed to a third-party manufacturer. With

luck, the furniture will be delivered to the customer’s home within

six to eight weeks. This is a value chain that maximizes

customization and service but does so at high cost.

In contrast, Ikea serves customers who are happy to trade off

service for cost. Instead of having a sales associate trail

customers around the store, Ikea uses a self-service model based on

clear, in-store displays. Rather than rely solely on third-party

manufacturers, Ikea designs its own low-cost, modular,

ready-to-assemble furniture to fit its positioning. In huge stores,

Ikea displays every product it sells in room-like settings, so

customers don’t need a decorator to help them imagine how to put the

pieces together. Adjacent to the furnished showrooms is a warehouse

section with the products in boxes on pallets. Customers are

expected to do their own pickup and delivery, and Ikea will even

sell you a roof rack for your car that you can return for a refund

on your next visit.

i

Although much of its low-cost position comes from having customers

“do it themselves,” Ikea offers a number of extra services that its

competitors do not. In-store child care is one. Extended hours are

another. Those services are uniquely aligned with the needs of its

customers, who are young, not wealthy, likely to have children (but

no nanny), and, because they work for a living, have a need to shop

at odd hours.

i

Strategic positions emerge from three distinct sources, which are

not mutually exclusive and often overlap. First, positioning can be

based on producing a subset of an industry’s products or services. I

call this variety-based positioning because it is based on the

choice of product or service varieties rather than customer

segments. Variety-based positioning makes economic sense when a

company can best produce particular products or services using

distinctive sets of activities.

Jiffy Lube International, for instance, specializes in automotive

lubricants and does not offer other car repair or maintenance

services. Its value chain produces faster service at a lower cost

than broader line repair shops, a combination so attractive that

many customers subdivide their purchases, buying oil changes from

the focused competitor, Jiffy Lube, and going to rivals for other

services.

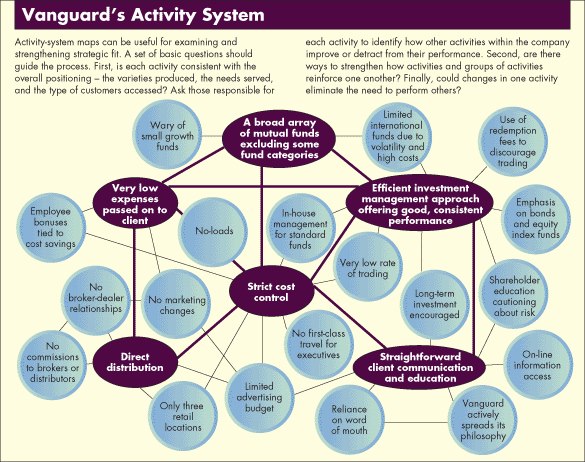

The Vanguard Group, a leader in the mutual fund industry, is another

example of variety-based positioning. Vanguard provides an array of

common stock, bond, and money market funds that offer predictable

performance and rock-bottom expenses. The company’s investment

approach deliberately sacrifices the possibility of extraordinary

performance in any one year for good relative performance in every

year. Vanguard is known, for example, for its index funds. It avoids

making bets on interest rates and steers clear of narrow stock

groups. Fund managers keep trading levels low, which holds expenses

down; in addition, the company discourages customers from rapid

buying and selling because doing so drives up costs and can force a

fund manager to trade in order to deploy new capital and raise cash

for redemptions. Vanguard also takes a consistent low-cost approach

to managing distribution, customer service, and marketing. Many

investors include one or more Vanguard funds in their portfolio,

while buying aggressively managed or specialized funds from

competitors.

The people who use Vanguard or Jiffy Lube are responding to a

superior value chain for a particular type of service. A

variety-based positioning can serve a wide array of customers, but

for most it will meet only a subset of their needs.

A second basis for positioning is that of serving most or all the

needs of a particular group of customers. I call this needs-based

positioning, which comes closer to traditional thinking about

targeting a segment of customers. It arises when there are groups of

customers with differing needs, and when a tailored set of

activities can serve those needs best. Some groups of customers are

more price sensitive than others, demand different product features,

and need varying amounts of information, support, and services.

Ikea’s customers are a good example of such a group. Ikea seeks to

meet all the home furnishing needs of its target customers, not just

a subset of them.

A variant of needs-based positioning arises when the same customer

has different needs on different occasions or for different types of

transactions. The same person, for example, may have different needs

when traveling on business than when traveling for pleasure with the

family. Buyers of cans—beverage companies, for example—will likely

have different needs from their primary supplier than from their

secondary source.

It is intuitive for most managers to conceive of their business in

terms of the customers’ needs they are meeting. But a critical

element of needs-based positioning is not at all intuitive and is

often overlooked. Differences in needs will not translate into

meaningful positions unless the best set of activities to satisfy

them also differs. If that were not the case, every competitor could

meet those same needs, and there would be nothing unique or valuable

about the positioning.

In private banking, for example, Bessemer Trust Company targets

families with a minimum of $5 million in investable assets who want

capital preservation combined with wealth accumulation. By assigning

one sophisticated account officer for every 14 families, Bessemer

has configured its activities for personalized service. Meetings,

for example, are more likely to be held at a client’s ranch or yacht

than in the office. Bessemer offers a wide array of customized

services, including investment management and estate administration,

oversight of oil and gas investments, and accounting for racehorses

and aircraft. Loans, a staple of most private banks, are rarely

needed by Bessemer’s clients and make up a tiny fraction of its

client balances and income. Despite the most generous compensation

of account officers and the highest personnel cost as a percentage

of operating expenses, Bessemer’s differentiation with its target

families produces a return on equity estimated to be the highest of

any private banking competitor.

Citibank’s private bank, on the other hand, serves clients with

minimum assets of about $250,000 who, in contrast to Bessemer’s

clients, want convenient access to loans—from jumbo mortgages to

deal financing. Citibank’s account managers are primarily lenders.

When clients need other services, their account manager refers them

to other Citibank specialists, each of whom handles prepackaged

products. Citibank’s system is less customized than Bessemer’s and

allows it to have a lower manager-to-client ratio of 1:125. Biannual

office meetings are offered only for the largest clients. Both

Bessemer and Citibank have tailored their activities to meet the

needs of a different group of private banking customers. The same

value chain cannot profitably meet the needs of both groups.

The third basis for positioning is that of segmenting customers who

are accessible in different ways. Although their needs are similar

to those of other customers, the best configuration of activities to

reach them is different. I call this access-based positioning.

Access can be a function of customer geography or customer scale—or

of anything that requires a different set of activities to reach

customers in the best way.

Segmenting by access is less common and less well understood than

the other two bases. Carmike Cinemas, for example, operates movie

theaters exclusively in cities and towns with populations under

200,000. How does Carmike make money in markets that are not only

small but also won’t support big-city ticket prices? It does so

through a set of activities that result in a lean cost structure.

Carmike’s small-town customers can be served through standardized,

low-cost theater complexes requiring fewer screens and less

sophisticated projection technology than big-city theaters. The

company’s proprietary information system and management process

eliminate the need for local administrative staff beyond a single

theater manager. Carmike also reaps advantages from centralized

purchasing, lower rent and payroll costs (because of its locations),

and rock-bottom corporate overhead of 2% (the industry average is

5%). Operating in small communities also allows Carmike to practice

a highly personal form of marketing in which the theater manager

knows patrons and promotes attendance through personal contacts. By

being the dominant if not the only theater in its markets—the main

competition is often the high school football team—Carmike is also

able to get its pick of films and negotiate better terms with

distributors.

Rural versus urban-based customers are one example of access driving

differences in activities. Serving small rather than large customers

or densely rather than sparsely situated customers are other

examples in which the best way to configure marketing, order

processing, logistics, and after-sale service activities to meet the

similar needs of distinct groups will often differ.

i

Positioning is not only about carving out a niche. A position

emerging from any of the sources can be broad or narrow. A focused

competitor, such as Ikea, targets the special needs of a subset of

customers and designs its activities accordingly. Focused

competitors thrive on groups of customers who are overserved (and

hence overpriced) by more broadly targeted competitors, or

underserved (and hence underpriced). A broadly targeted

competitor—for example, Vanguard or Delta Air Lines—serves a wide

array of customers, performing a set of activities designed to meet

their common needs. It ignores or meets only partially the more

idiosyncratic needs of particular customer customer groups.

Whatever the basis—variety, needs, access, or some combination of

the three—positioning requires a tailored set of activities because

it is always a function of differences on the supply side; that is,

of differences in activities. However, positioning is not always a

function of differences on the demand, or customer, side. Variety

and access positionings, in particular, do not rely on any customer

differences. In practice, however, variety or access differences

often accompany needs differences. The tastes—that is, the needs—of

Carmike’s small-town customers, for instance, run more toward

comedies, Westerns, action films, and family entertainment. Carmike

does not run any films rated NC-17.

Having defined positioning, we can now begin to answer the question,

“What is strategy?” Strategy is the creation of a unique and

valuable position, involving a different set of activities. If there

were only one ideal position, there would be no need for strategy.

Companies would face a simple imperative—win the race to discover

and preempt it. The essence of strategic positioning is to choose

activities that are different from rivals’. If the same set of

activities were best to produce all varieties, meet all needs, and

access all customers, companies could easily shift among them and

operational effectiveness would determine performance.

i

Choosing a unique position, however, is not enough to guarantee a

sustainable advantage. A valuable position will attract imitation by

incumbents, who are likely to copy it in one of two ways.

First, a competitor can reposition itself to match the superior

performer. J.C. Penney, for instance, has been repositioning itself

from a Sears clone to a more upscale, fashion-oriented, soft-goods

retailer. A second and far more common type of imitation is

straddling. The straddler seeks to match the benefits of a

successful position while maintaining its existing position. It

grafts new features, services, or technologies onto the activities

it already performs.

For those who argue that competitors can copy any market position,

the airline industry is a perfect test case. It would seem that

nearly any competitor could imitate any other airline’s activities.

Any airline can buy the same planes, lease the gates, and match the

menus and ticketing and baggage handling services offered by other

airlines.

Continental Airlines saw how well Southwest was doing and decided to

straddle. While maintaining its position as a full-service airline,

Continental also set out to match Southwest on a number of

point-to-point routes. The airline dubbed the new service

Continental Lite. It eliminated meals and first-class service,

increased departure frequency, lowered fares, and shortened

turnaround time at the gate. Because Continental remained a

full-service airline on other routes, it continued to use travel

agents and its mixed fleet of planes and to provide baggage checking

and seat assignments.

But a strategic position is not sustainable unless there are

trade-offs with other positions. Trade-offs occur when activities

are incompatible. Simply put, a trade-off means that more of one

thing necessitates less of another. An airline can choose to serve

meals—adding cost and slowing turnaround time at the gate—or it can

choose not to, but it cannot do both without bearing major

inefficiencies.

Trade-offs create the need for choice and protect against

repositioners and straddlers. Consider Neutrogena soap. Neutrogena

Corporation’s variety-based positioning is built on a “kind to the

skin,” residue-free soap formulated for pH balance. With a large

detail force calling on dermatologists, Neutrogena’s marketing

strategy looks more like a drug company’s than a soap maker’s. It

advertises in medical journals, sends direct mail to doctors,

attends medical conferences, and performs research at its own

Skincare Institute. To reinforce its positioning, Neutrogena

originally focused its distribution on drugstores and avoided price

promotions. Neutrogena uses a slow, more expensive manufacturing

process to mold its fragile soap.

In choosing this position, Neutrogena said no to the deodorants and

skin softeners that many customers desire in their soap. It gave up

the large-volume potential of selling through supermarkets and using

price promotions. It sacrificed manufacturing efficiencies to

achieve the soap’s desired attributes. In its original positioning,

Neutrogena made a whole raft of trade-offs like those, trade-offs

that protected the company from imitators.

Trade-offs arise for three reasons. The first is inconsistencies in

image or reputation. A company known for delivering one kind of

value may lack credibility and confuse customers—or even undermine

its reputation—if it delivers another kind of value or attempts to

deliver two inconsistent things at the same time. For example, Ivory

soap, with its position as a basic, inexpensive everyday soap would

have a hard time reshaping its image to match Neutrogena’s premium

“medical” reputation. Efforts to create a new image typically cost

tens or even hundreds of millions of dollars in a major industry—a

powerful barrier to imitation.

Second, and more important, trade-offs arise from activities

themselves. Different positions (with their tailored activities)

require different product configurations, different equipment,

different employee behavior, different skills, and different

management systems. Many trade-offs reflect inflexibilities in

machinery, people, or systems. The more Ikea has configured its

activities to lower costs by having its customers do their own

assembly and delivery, the less able it is to satisfy customers who

require higher levels of service.

However, trade-offs can be even more basic. In general, value is

destroyed if an activity is overdesigned or underdesigned for its

use. For example, even if a given salesperson were capable of

providing a high level of assistance to one customer and none to

another, the salesperson’s talent (and some of his or her cost)

would be wasted on the second customer. Moreover, productivity can

improve when variation of an activity is limited. By providing a

high level of assistance all the time, the salesperson and the

entire sales activity can often achieve efficiencies of learning and

scale.

Finally, trade-offs arise from limits on internal coordination and

control. By clearly choosing to compete in one way and not another,

senior management makes organizational priorities clear. Companies

that try to be all things to all customers, in contrast, risk

confusion in the trenches as employees attempt to make day-to-day

operating decisions without a clear framework.

Positioning trade-offs are pervasive in competition and essential to

strategy. They create the need for choice and purposefully limit

what a company offers. They deter straddling or repositioning,

because competitors that engage in those approaches undermine their

strategies and degrade the value of their existing activities.

Trade-offs ultimately grounded Continental Lite. The airline lost

hundreds of millions of dollars, and the CEO lost his job. Its

planes were delayed leaving congested hub cities or slowed at the

gate by baggage transfers. Late flights and cancellations generated

a thousand complaints a day. Continental Lite could not afford to

compete on price and still pay standard travel-agent commissions,

but neither could it do without agents for its full-service

business. The airline compromised by cutting commissions for all

Continental flights across the board. Similarly, it could not afford

to offer the same frequent-flier benefits to travelers paying the

much lower ticket prices for Lite service. It compromised again by

lowering the rewards of Continental’s entire frequent-flier program.

The results: angry travel agents and full-service customers.

Continental tried to compete in two ways at once. In trying to be

low cost on some routes and full service on others, Continental paid

an enormous straddling penalty. If there were no trade-offs between

the two positions, Continental could have succeeded. But the absence

of trade-offs is a dangerous half-truth that managers must unlearn.

Quality is not always free. Southwest’s convenience, one kind of

high quality, happens to be consistent with low costs because its

frequent departures are facilitated by a number of low-cost

practices—fast gate turnarounds and automated ticketing, for

example. However, other dimensions of airline quality—an assigned

seat, a meal, or baggage transfer—require costs to provide.

In general, false trade-offs between cost and quality occur

primarily when there is redundant or wasted effort, poor control or

accuracy, or weak coordination. Simultaneous improvement of cost and

differentiation is possible only when a company begins far behind

the productivity frontier or when the frontier shifts outward. At

the frontier, where companies have achieved current best practice,

the trade-off between cost and differentiation is very real indeed.

After a decade of enjoying productivity advantages, Honda Motor

Company and Toyota Motor Corporation recently bumped up against the

frontier. In 1995, faced with increasing customer resistance to

higher automobile prices, Honda found that the only way to produce a

less-expensive car was to skimp on features. In the United States,

it replaced the rear disk brakes on the Civic with lower-cost drum

brakes and used cheaper fabric for the back seat, hoping customers

would not notice. Toyota tried to sell a version of its best-selling

Corolla in Japan with unpainted bumpers and cheaper seats. In

Toyota’s case, customers rebelled, and the company quickly dropped

the new model.

For the past decade, as managers have improved operational

effectiveness greatly, they have internalized the idea that

eliminating trade-offs is a good thing. But if there are no

trade-offs companies will never achieve a sustainable advantage.

They will have to run faster and faster just to stay in place.

As we return to the question, What is strategy? we see that

trade-offs add a new dimension to the answer. Strategy is making

trade-offs in competing. The essence of strategy is choosing what

not to do. Without trade-offs, there would be no need for choice and

thus no need for strategy. Any good idea could and would be quickly

imitated. Again, performance would once again depend wholly on

operational effectiveness.

i

Positioning choices determine not only which activities a company

will perform and how it will configure individual activities but

also how activities relate to one another. While operational

effectiveness is about achieving excellence in individual

activities, or functions, strategy is about combining activities.

Southwest’s rapid gate turnaround, which allows frequent departures

and greater use of aircraft, is essential to its high-convenience,

low-cost positioning. But how does Southwest achieve it? Part of the

answer lies in the company’s well-paid gate and ground crews, whose

productivity in turnarounds is enhanced by flexible union rules. But

the bigger part of the answer lies in how Southwest performs other

activities. With no meals, no seat assignment, and no interline

baggage transfers, Southwest avoids having to perform activities

that slow down other airlines. It selects airports and routes to

avoid congestion that introduces delays. Southwest’s strict limits

on the type and length of routes make standardized aircraft

possible: every aircraft Southwest turns is a Boeing 737.

What is Southwest’s core competence? Its key success factors? The

correct answer is that everything matters. Southwest’s strategy

involves a whole system of activities, not a collection of parts.

Its competitive advantage comes from the way its activities fit and

reinforce one another.

Fit locks out imitators by creating a chain that is as strong as its

strongest link. As in most companies with good strategies,

Southwest’s activities complement one another in ways that create

real economic value. One activity’s cost, for example, is lowered

because of the way other activities are performed. Similarly, one

activity’s value to customers can be enhanced by a company’s other

activities. That is the way strategic fit creates competitive

advantage and superior profitability.

i

The importance of fit among functional policies is one of the oldest

ideas in strategy. Gradually, however, it has been supplanted on the

management agenda. Rather than seeing the company as a whole,

managers have turned to “core” competencies, “critical” resources,

and “key” success factors. In fact, fit is a far more central

component of competitive advantage than most realize.

Fit is important because discrete activities often affect one

another. A sophisticated sales force, for example, confers a greater

advantage when the company’s product embodies premium technology and

its marketing approach emphasizes customer assistance and support. A

production line with high levels of model variety is more valuable

when combined with an inventory and order processing system that

minimizes the need for stocking finished goods, a sales process

equipped to explain and encourage customization, and an advertising

theme that stresses the benefits of product variations that meet a

customer’s special needs. Such complementarities are pervasive in

strategy. Although some fit among activities is generic and applies

to many companies, the most valuable fit is strategy-specific

because it enhances a position’s uniqueness and amplifies

trade-offs.2

There are three types of fit, although they are not mutually

exclusive. First-order fit is simple consistency between each

activity (function) and the overall strategy. Vanguard, for example,

aligns all activities with its low-cost strategy. It minimizes

portfolio turnover and does not need highly compensated money

managers. The company distributes its funds directly, avoiding

commissions to brokers. It also limits advertising, relying instead

on public relations and word-of-mouth recommendations. Vanguard ties

its employees’ bonuses to cost savings.

Consistency ensures that the competitive advantages of activities

cumulate and do not erode or cancel themselves out. It makes the

strategy easier to communicate to customers, employees, and

shareholders, and improves implementation through single-mindedness

in the corporation.

Second-order fit occurs when activities are reinforcing. Neutrogena,

for example, markets to upscale hotels eager to offer their guests a

soap recommended by dermatologists. Hotels grant Neutrogena the

privilege of using its customary packaging while requiring other

soaps to feature the hotel’s name. Once guests have tried Neutrogena

in a luxury hotel, they are more likely to purchase it at the

drugstore or ask their doctor about it. Thus Neutrogena’s medical

and hotel marketing activities reinforce one another, lowering total

marketing costs.

In another example, Bic Corporation sells a narrow line of standard,

low-priced pens to virtually all major customer markets (retail,

commercial, promotional, and giveaway) through virtually all

available channels. As with any variety-based positioning serving a

broad group of customers, Bic emphasizes a common need (low price

for an acceptable pen) and uses marketing approaches with a broad

reach (a large sales force and heavy television advertising). Bic

gains the benefits of consistency across nearly all activities,

including product design that emphasizes ease of manufacturing,

plants configured for low cost, aggressive purchasing to minimize

material costs, and in-house parts production whenever the economics

dictate.

Yet Bic goes beyond simple consistency because its activities are

reinforcing. For example, the company uses point-of-sale displays

and frequent packaging changes to stimulate impulse buying. To

handle point-of-sale tasks, a company needs a large sales force.

Bic’s is the largest in its industry, and it handles point-of-sale

activities better than its rivals do. Moreover, the combination of

point-of-sale activity, heavy television advertising, and packaging

changes yields far more impulse buying than any activity in

isolation could.

Third-order fit goes beyond activity reinforcement to what I call

optimization of effort. The Gap, a retailer of casual clothes,

considers product availability in its stores a critical element of

its strategy. The Gap could keep products either by holding store

inventory or by restocking from warehouses. The Gap has optimized

its effort across these activities by restocking its selection of

basic clothing almost daily out of three warehouses, thereby

minimizing the need to carry large in-store inventories. The

emphasis is on restocking because the Gap’s merchandising strategy

sticks to basic items in relatively few colors. While comparable

retailers achieve turns of three to four times per year, the Gap

turns its inventory seven and a half times per year. Rapid

restocking, moreover, reduces the cost of implementing the Gap’s

short model cycle, which is six to eight weeks long.3

Coordination and information exchange across activities to eliminate

redundancy and minimize wasted effort are the most basic types of

effort optimization. But there are higher levels as well. Product

design choices, for example, can eliminate the need for after-sale

service or make it possible for customers to perform service

activities themselves. Similarly, coordination with suppliers or

distribution channels can eliminate the need for some in-house

activities, such as end-user training.

In all three types of fit, the whole matters more than any

individual part. Competitive advantage grows out of the entire

system of activities. The fit among activities substantially reduces

cost or increases differentiation. Beyond that, the competitive

value of individual activities—or the associated skills,

competencies, or resources—cannot be decoupled from the system or

the strategy. Thus in competitive companies it can be misleading to

explain success by specifying individual strengths, core

competencies, or critical resources. The list of strengths cuts

across many functions, and one strength blends into others. It is

more useful to think in terms of themes that pervade many

activities, such as low cost, a particular notion of customer

service, or a particular conception of the value delivered. These

themes are embodied in nests of tightly linked activities.

i

Strategic fit among many activities is fundamental not only to

competitive advantage but also to the sustainability of that

advantage. It is harder for a rival to match an array of interlocked

activities than it is merely to imitate a particular sales-force

approach, match a process technology, or replicate a set of product

features. Positions built on systems of activities are far more

sustainable than those built on individual activities.

Consider this simple exercise. The probability that competitors can

match any activity is often less than one. The probabilities then

quickly compound to make matching the entire system highly unlikely

(.9 × .9 = .81; .9 × .9 × .9 × .9 = .66, and so on). Existing

companies that try to reposition or straddle will be forced to

reconfigure many activities. And even new entrants, though they do

not confront the trade-offs facing established rivals, still face

formidable barriers to imitation.

The more a company’s positioning rests on activity systems with

second- and third-order fit, the more sustainable its advantage will

be. Such systems, by their very nature, are usually difficult to

untangle from outside the company and therefore hard to imitate. And

even if rivals can identify the relevant interconnections, they will

have difficulty replicating them. Achieving fit is difficult because

it requires the integration of decisions and actions across many

independent subunits.

A competitor seeking to match an activity system gains little by

imitating only some activities and not matching the whole.

Performance does not improve; it can decline. Recall Continental

Lite’s disastrous attempt to imitate Southwest.

Finally, fit among a company’s activities creates pressures and

incentives to improve operational effectiveness, which makes

imitation even harder. Fit means that poor performance in one

activity will degrade the performance in others, so that weaknesses

are exposed and more prone to get attention. Conversely,

improvements in one activity will pay dividends in others. Companies

with strong fit among their activities are rarely inviting targets.

Their superiority in strategy and in execution only compounds their

advantages and raises the hurdle for imitators.

i

When activities complement one another, rivals will get little

benefit from imitation unless they successfully match the whole

system. Such situations tend to promote winner-take-all competition.

The company that builds the best activity system—Toys R Us, for

instance—wins, while rivals with similar strategies—Child World and

Lionel Leisure—fall behind. Thus finding a new strategic position is

often preferable to being the second or third imitator of an

occupied position.

The most viable positions are those whose activity systems are

incompatible because of tradeoffs. Strategic positioning sets the

trade-off rules that define how individual activities will be

configured and integrated. Seeing strategy in terms of activity

systems only makes it clearer why organizational structure, systems,

and processes need to be strategy-specific. Tailoring organization

to strategy, in turn, makes complementarities more achievable and

contributes to sustainability.

One implication is that strategic positions should have a horizon of

a decade or more, not of a single planning cycle. Continuity fosters

improvements in individual activities and the fit across activities,

allowing an organization to build unique capabilities and skills

tailored to its strategy. Continuity also reinforces a company’s

identity.

Conversely, frequent shifts in positioning are costly. Not only must

a company reconfigure individual activities, but it must also

realign entire systems. Some activities may never catch up to the

vacillating strategy. The inevitable result of frequent shifts in

strategy, or of failure to choose a distinct position in the first

place, is “me-too” or hedged activity configurations,

inconsistencies across functions, and organizational dissonance.

What is strategy? We can now complete the answer to this question.

Strategy is creating fit among a company’s activities. The success

of a strategy depends on doing many things well—not just a few—and

integrating among them. If there is no fit among activities, there

is no distinctive strategy and little sustainability. Management

reverts to the simpler task of overseeing independent functions, and

operational effectiveness determines an organization’s relative

performance.

i

Why do so many companies fail to have a strategy? Why do managers

avoid making strategic choices? Or, having made them in the past,

why do managers so often let strategies decay and blur?

Commonly, the threats to strategy are seen to emanate from outside a

company because of changes in technology or the behavior of

competitors. Although external changes can be the problem, the

greater threat to strategy often comes from within. A sound strategy

is undermined by a misguided view of competition, by organizational

failures, and, especially, by the desire to grow.

Managers have become confused about the necessity of making choices.

When many companies operate far from the productivity frontier,

trade-offs appear unnecessary. It can seem that a well-run company

should be able to beat its ineffective rivals on all dimensions

simultaneously. Taught by popular management thinkers that they do

not have to make trade-offs, managers have acquired a macho sense

that to do so is a sign of weakness.

Unnerved by forecasts of hypercompetition, managers increase its

likelihood by imitating everything about their competitors. Exhorted

to think in terms of revolution, managers chase every new technology

for its own sake.

The pursuit of operational effectiveness is seductive because it is

concrete and actionable. Over the past decade, managers have been

under increasing pressure to deliver tangible, measurable

performance improvements. Programs in operational effectiveness

produce reassuring progress, although superior profitability may

remain elusive. Business publications and consultants flood the

market with information about what other companies are doing,

reinforcing the best-practice mentality. Caught up in the race for

operational effectiveness, many managers simply do not understand

the need to have a strategy.

Companies avoid or blur strategic choices for other reasons as well.

Conventional wisdom within an industry is often strong, homogenizing

competition. Some managers mistake “customer focus” to mean they

must serve all customer needs or respond to every request from

distribution channels. Others cite the desire to preserve

flexibility.

Organizational realities also work against strategy. Trade-offs are

frightening, and making no choice is sometimes preferred to risking

blame for a bad choice. Companies imitate one another in a type of

herd behavior, each assuming rivals know something they do not.

Newly empowered employees, who are urged to seek every possible

source of improvement, often lack a vision of the whole and the

perspective to recognize trade-offs. The failure to choose sometimes

comes down to the reluctance to disappoint valued managers or

employees.

i

Among all other influences, the desire to grow has perhaps the most

perverse effect on strategy. Trade-offs and limits appear to

constrain growth. Serving one group of customers and excluding

others, for instance, places a real or imagined limit on revenue

growth. Broadly targeted strategies emphasizing low price result in

lost sales with customers sensitive to features or service.

Differentiators lose sales to price-sensitive customers.

Managers are constantly tempted to take incremental steps that

surpass those limits but blur a company’s strategic position.

Eventually, pressures to grow or apparent saturation of the target

market lead managers to broaden the position by extending product

lines, adding new features, imitating competitors’ popular services,

matching processes, and even making acquisitions. For years, Maytag

Corporation’s success was based on its focus on reliable, durable

washers and dryers, later extended to include dishwashers. However,

conventional wisdom emerging within the industry supported the

notion of selling a full line of products. Concerned with slow

industry growth and competition from broad-line appliance makers,

Maytag was pressured by dealers and encouraged by customers to

extend its line. Maytag expanded into refrigerators and cooking

products under the Maytag brand and acquired other brands—Jenn-Air,

Hardwick Stove, Hoover, Admiral, and Magic Chef—with disparate

positions. Maytag has grown substantially from $684 million in 1985

to a peak of $3.4 billion in 1994, but return on sales has declined

from 8% to 12% in the 1970s and 1980s to an average of less than 1%

between 1989 and 1995. Cost cutting will improve this performance,

but laundry and dishwasher products still anchor Maytag’s

profitability.

i

Neutrogena may have fallen into the same trap. In the early 1990s,

its U.S. distribution broadened to include mass merchandisers such

as Wal-Mart Stores. Under the Neutrogena name, the company expanded

into a wide variety of products—eye-makeup remover and shampoo, for

example—in which it was not unique and which diluted its image, and

it began turning to price promotions.

Compromises and inconsistencies in the pursuit of growth will erode

the competitive advantage a company had with its original varieties

or target customers. Attempts to compete in several ways at once

create confusion and undermine organizational motivation and focus.

Profits fall, but more revenue is seen as the answer. Managers are

unable to make choices, so the company embarks on a new round of

broadening and compromises. Often, rivals continue to match each

other until desperation breaks the cycle, resulting in a merger or

downsizing to the original positioning.

i

Many companies, after a decade of restructuring and cost-cutting,

are turning their attention to growth. Too often, efforts to grow

blur uniqueness, create compromises, reduce fit, and ultimately

undermine competitive advantage. In fact, the growth imperative is

hazardous to strategy.

What approaches to growth preserve and reinforce strategy? Broadly,

the prescription is to concentrate on deepening a strategic position

rather than broadening and compromising it. One approach is to look

for extensions of the strategy that leverage the existing activity

system by offering features or services that rivals would find

impossible or costly to match on a stand-alone basis. In other

words, managers can ask themselves which activities, features, or

forms of competition are feasible or less costly to them because of

complementary activities that their company performs.

Deepening a position involves making the company’s activities more

distinctive, strengthening fit, and communicating the strategy

better to those customers who should value it. But many companies

succumb to the temptation to chase “easy” growth by adding hot

features, products, or services without screening them or adapting

them to their strategy. Or they target new customers or markets in

which the company has little special to offer. A company can often

grow faster—and far more profitably—by better penetrating needs and

varieties where it is distinctive than by slugging it out in

potentially higher growth arenas in which the company lacks

uniqueness. Carmike, now the largest theater chain in the United

States, owes its rapid growth to its disciplined concentration on

small markets. The company quickly sells any big-city theaters that

come to it as part of an acquisition.

Globalization often allows growth that is consistent with strategy,

opening up larger markets for a focused strategy. Unlike broadening

domestically, expanding globally is likely to leverage and reinforce

a company’s unique position and identity.

Companies seeking growth through broadening within their industry

can best contain the risks to strategy by creating stand-alone

units, each with its own brand name and tailored activities. Maytag

has clearly struggled with this issue. On the one hand, it has

organized its premium and value brands into separate units with

different strategic positions. On the other, it has created an

umbrella appliance company for all its brands to gain critical mass.

With shared design, manufacturing, distribution, and customer

service, it will be hard to avoid homogenization. If a given

business unit attempts to compete with different positions for

different products or customers, avoiding compromise is nearly

impossible.

i

The challenge of developing or reestablishing a clear strategy is

often primarily an organizational one and depends on leadership.

With so many forces at work against making choices and tradeoffs in

organizations, a clear intellectual framework to guide strategy is a

necessary counterweight. Moreover, strong leaders willing to make

choices are essential.

In many companies, leadership has degenerated into orchestrating

operational improvements and making deals. But the leader’s role is

broader and far more important. General management is more than the

stewardship of individual functions. Its core is strategy: defining

and communicating the company’s unique position, making trade-offs,

and forging fit among activities. The leader must provide the

discipline to decide which industry changes and customer needs the

company will respond to, while avoiding organizational distractions

and maintaining the company’s distinctiveness. Managers at lower

levels lack the perspective and the confidence to maintain a

strategy. There will be constant pressures to compromise, relax

trade-offs, and emulate rivals. One of the leader’s jobs is to teach

others in the organization about strategy—and to say no.

Strategy renders choices about what not to do as important as

choices about what to do. Indeed, setting limits is another function

of leadership. Deciding which target group of customers, varieties,

and needs the company should serve is fundamental to developing a

strategy. But so is deciding not to serve other customers or needs

and not to offer certain features or services. Thus strategy

requires constant discipline and clear communication. Indeed, one of

the most important functions of an explicit, communicated strategy

is to guide employees in making choices that arise because of

trade-offs in their individual activities and in day-to-day

decisions.

Michael E. Porter is the C. Roland Christensen Professor of Business

Administration at the Harvard Business School in Boston,

Massachusetts.

i

TACS Science

Technology Engineering and Consulting Delivers The Insight and Vision on Information

Communication and Energy Technologies for Strategic Decisions.

TACS is Pioneer and Innovator of many Communication Signal

Processors, Optical Modems, Optimum or Robust Multi-User or

Single-User MIMO Packet Radio Modems, 1G Modems, 2G Modems, 3G

Modems, 4G Modems, 5G Modems, 6G Modems, Satellite Modems, PSTN

Modems, Cable Modems, PLC Modems, IoT Modems and more..

TACS scientists engineers and consultants conducted fundamental scientific research in

the field of communications and are the pioneer and first

inventors of PLC MODEMS, Optimum or Robust Multi-User or

Single-User MIMO fixed or mobile packet radio structures in the

world.

TACS is a leading concept technology provider and top

science technology engineering and consultancy in the field of Information,

Communication and Energy Technologies (ICET). The heart of our

Consulting spectrum comprises strategic, organizational, and

technology-intensive tasks that arise from the use of new

information and telecommunications technologies. TACS Science

Technology Engineering and Consulting

offers Strategic Planning, Information, Communications and

Energy Technology Standards and Architecture Assessment, Systems

Engineering, Planning, and Resource Optimization.

TACS is a leading top consultancy in the field of information, communication

and energy technologies (ICET).

The heart of our consulting spectrum comprises strategic,

organizational, and technology-intensive tasks that arise from the use of new

information, communication and energy technologies.

The major emphasis in our work is found in innovative consulting and

implementation solutions which result from the use of modern information,

communication and energy technologies.

TACS

Delivers the insight and vision

on technology for strategic decisions

Drives

innovations forward as part of our service offerings to customers

worldwide

Conceives

integral solutions on the basis of our integrated business and technological

competence in the ICET sector

Assesses technologies and standards and develops

architectures for fixed or mobile, wired or wireless communications systems

and networks

Provides

the energy and experience of world-wide leading innovators and experts in their fields for local,

national or large-scale international projects.